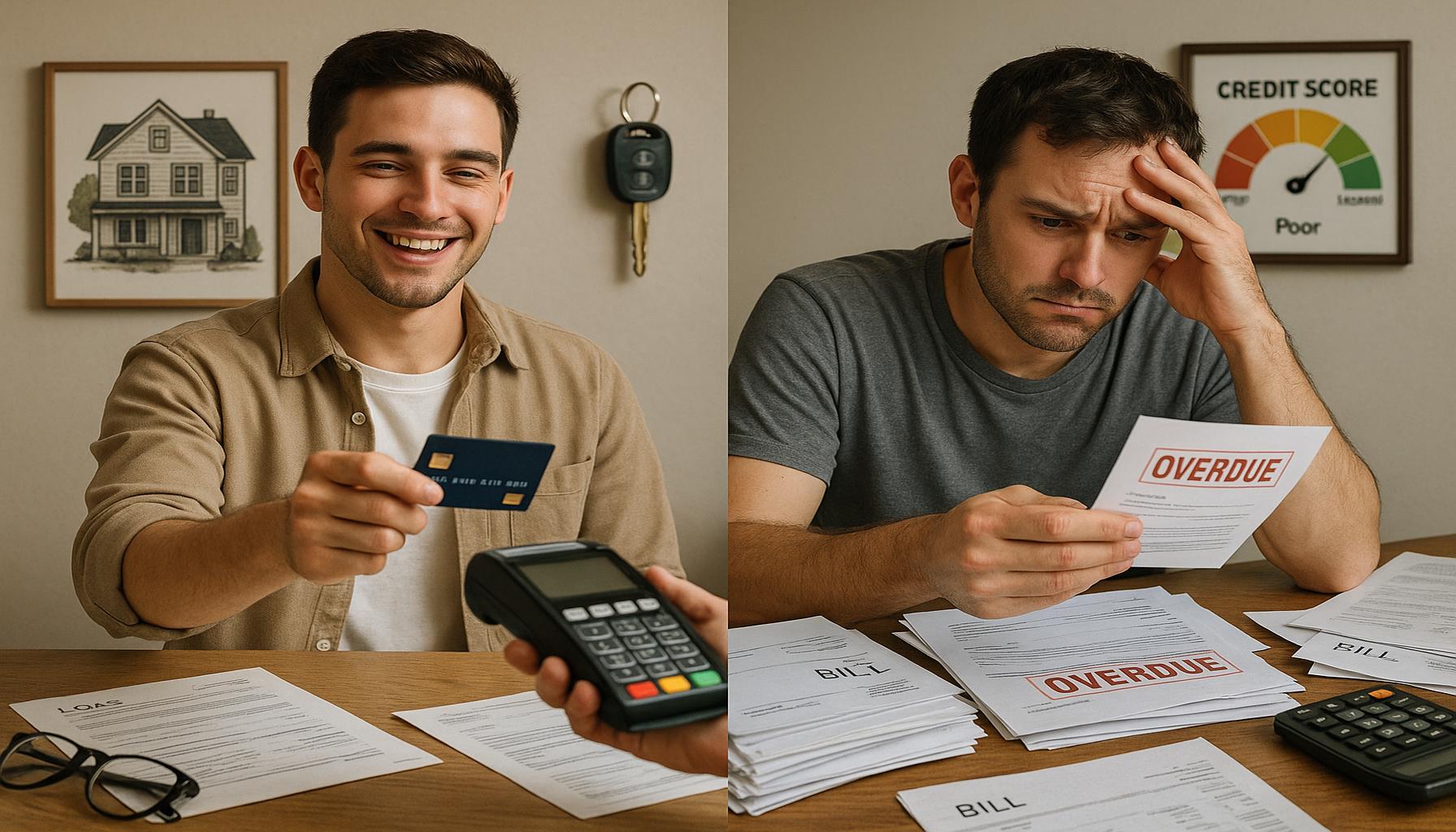

The Benefits and Disadvantages of Using Credit Cards to Build a Credit History

Credit cards can be seen as a powerful financial tool for consumers. When used wisely, they can pave the way to a stable credit history that can open doors to numerous financial opportunities, such as loans for homes, cars, or even favorable insurance rates. However, understanding the dual nature of credit cards is crucial, as mismanagement can lead to substantial financial setbacks.

Benefits of Using Credit Cards

- Improving Your Credit Score: One of the primary benefits of using credit cards is the positive impact on your credit score. Credit scores are determined by several factors, with payment history being the most significant. By making consistent, on-time payments, you can help raise your score over time. For instance, if you have a credit card with a $500 limit and regularly pay the balance in full by the due date, this responsible use demonstrates to lenders that you are a reliable borrower, which can result in a higher credit score.

- Convenience: Credit cards offer unmatched convenience. Whether you are making everyday purchases at the grocery store or booking a last-minute flight, credit cards can expedite transactions. Additionally, credit cards can be invaluable in emergency situations. For example, if your car breaks down unexpectedly, having a credit card can allow you to cover repair costs without needing to deplete your savings immediately.

- Rewards Programs: Many credit cards come with enticing rewards programs. These programs may offer cashback on purchases, travel points, or discounts at specific retailers. For example, a card that offers 2% cashback on all purchases can effectively translate into savings over time. If you spend $1,000 in a year, you would earn $20 in cashback, which can be considered a nice bonus for your regular spending.

Disadvantages of Using Credit Cards

- High Interest Rates: While credit cards can help build your credit, they often come with high-interest rates on outstanding balances. If you carry a balance month to month without paying it off in full, the interest can compound quickly. For instance, with an average credit card interest rate of around 16%, a $1,000 balance could lead to over $160 in interest charges if left unpaid for a year.

- Risk of Overspending: The convenience of credit cards can lead many individuals to overspend. The ability to swipe a card rather than handing over cash creates a disconnect with your budget. For example, someone might buy a new television they don’t necessarily need simply because they feel they can manage the payment later, which can lead to accumulating debt that impacts their financial stability.

- Impact on Credit Score: Mismanagement of credit cards can also detrimentally affect your credit score. Missed payments, high credit utilization (meaning utilizing a significant portion of your credit limit), and numerous hard inquiries can all lower your score. For instance, if you frequently max out your card and fail to pay on time, this behavior can lead to a decrease in your creditworthiness and hurt future lending opportunities.

By understanding these factors, individuals can make more informed decisions about their financial futures. With careful management, credit cards can be a helpful asset to enhance your credit history. However, it’s essential to remain vigilant about spending habits and payment schedules to avoid the pitfalls that result from mishandling credit.

EXPLORE MORE: Click here for insights on how cost of living influences financial choices

Understanding the Balance: Benefits of Credit Cards

When it comes to building a solid credit history, utilizing credit cards can serve as an effective strategy. However, their benefits go beyond just improving your credit score. Here are several reasons why credit cards can be advantageous:

- Improving Your Credit Score: One of the primary benefits of using credit cards is their ability to positively impact your credit score. Credit scores are determined by multiple factors, with payment history being the most significant. By consistently making on-time payments, you can gradually raise your score. For instance, if you have a credit card with a $500 limit and pay off the balance each month by the due date, you demonstrate reliability as a borrower. This responsible use can lead to a higher credit score over time, enhancing your chances of loan approvals in the future.

- Convenience: Credit cards offer unparalleled convenience in the modern economy. They simplify transactions, allowing you to make purchases easily whether you are at a local grocery store, dining out, or shopping online. Moreover, credit cards can provide a financial safety net in emergencies. For example, if your car suddenly requires expensive repairs, you can cover the costs using a credit card without immediately impacting your savings account.

- Rewards Programs: Many credit cards also feature rewards programs that can be quite enticing. These programs often provide cashback on purchases, travel points that can be redeemed for trips, or discounts at affiliated retailers. For example, a credit card that offers 1.5% cashback on every dollar spent can lead to significant savings. If you spend $2,000 in a year, that translates into $30 of cashback, essentially giving you a bonus simply for using your card to make everyday purchases.

- Builds Credit History: Using credit cards regularly and responsibly can help you establish a credit history, which is crucial when you apply for loans or mortgages in the future. Lenders like to see a history of successful credit management, and regular use of a credit card followed by reliable payments can illustrate your ability to handle credit responsibly. This can be a vital advantage when applying for significant loans.

Understanding the Balance: Disadvantages of Credit Cards

While credit cards offer several benefits, they also come with certain disadvantages that can pose challenges. Being aware of these potential pitfalls is crucial for managing your financial health effectively:

- High Interest Rates: Many credit cards charge high-interest rates on unpaid balances. If you do not pay off your card in full each month, the interest can quickly accumulate. For instance, if your card has an interest rate of 18% and you carry a balance of $1,000, you may be responsible for around $180 in interest after a year. This can lead to a cycle of debt that becomes difficult to manage.

- Risk of Overspending: The convenience of credit cards can sometimes lead to overspending. When you have a credit card, it can feel easier to make impulsive purchases without fully assessing your budget. For example, someone might buy new clothing or electronics that exceed their budget just because they can pay with a card, leading to unnecessary debt that strains their finances over time.

- Impact on Credit Score: Mismanagement of credit cards can adversely affect your credit score. Late payments, high credit utilization (using a large portion of your credit limit), and multiple hard inquiries can all contribute to a decrease in your score. For instance, if you frequently max out your card and miss payment deadlines, these behaviors can damage your creditworthiness, which may hinder your future lending opportunities.

Understanding the balance between the advantages and disadvantages of credit cards can empower individuals to make informed decisions about their financial future. With careful management and a clear budget, credit cards can be a powerful asset in building your credit history.

DIVE DEEPER: Click here to discover more insights

Strategic Considerations: Navigating the Risks of Credit Cards

As we delve deeper into the topic, it’s essential to recognize that while credit cards can be beneficial in building credit history, they also introduce certain risks and challenges. Understanding these nuances can help consumers make more informed financial decisions. Here are several additional disadvantages to consider:

- Fees and Charges: Many credit cards come with various fees that can quickly add up if you’re not careful. Common fees include annual fees, late payment fees, and foreign transaction fees. For instance, if your credit card has a $100 annual fee and you forget to make a payment on time, adding a late fee of $39, your costs can grow significantly in just one year. This might negate the benefits you hoped to gain from using the card responsibly.

- Complex Terms and Conditions: Credit card agreements can often be complicated, with varied interest rates, limits, and rewards structures. Many consumers may not fully understand how these terms affect their usage. For example, some reward programs may only offer benefits after reaching a certain spending threshold or may have expiration dates that can lead to lost rewards if not closely monitored. This complexity can undermine the overall benefits of using credit cards.

- Potential for Identity Theft: Credit cards can expose you to the risk of identity theft, especially if sensitive information is not well-protected. If someone obtains your card information, they could make unauthorized purchases that you are liable for, causing a negative impact on your credit history. For example, if an identity thief runs up charges totaling $5,000 on your account before you notice, it may take significant time to resolve the issue and could lead to payment delinquency or decreased credit scores during that time.

- Future Borrowing Impact: Credit card usage can also affect your ability to secure future loans, particularly if you carry high balances. Lenders assess your credit utilization ratio, which compares your credit card balances to your credit limits. If you are consistently using a large percentage of your available credit, it can signal to lenders that you may be financially overextended. For example, if you have a total credit limit of $10,000 but regularly carry a balance of $8,000, your credit utilization ratio would be 80%, a level that can be considered risky by potential lenders.

- Emotional Spending Habits: Credit cards can sometimes lead to emotional spending, where individuals make purchases based on feelings rather than necessity. For example, someone might indulge in retail therapy after a rough day at work, leading to impulsive buying. This behavior not only adds to debt but can also distort the notion of responsible credit usage, complicating the effort to build a positive credit history.

Weighing these disadvantages against the benefits of credit cards is crucial for effective financial planning. By understanding the potential downsides, consumers can adopt strategies that mitigate risks, ensuring that their credit-building endeavors remain on a path towards financial stability and success.

DISCOVER MORE: Click here to learn how to apply

Final Thoughts on Building Credit History with Credit Cards

In conclusion, utilizing credit cards as a means to build a credit history can be a double-edged sword. On one hand, credit cards offer significant benefits, such as establishing a strong credit score, providing rewards, and enhancing financial flexibility. Responsible usage, including timely payments and maintaining a low credit utilization ratio, can pave the way for favorable borrowing conditions in the future.

However, it is equally important to acknowledge the disadvantages and pitfalls associated with credit card use. Fees, complex terms, identity theft risks, and the temptation of emotional spending can all negatively impact your financial health if not managed carefully. Understanding these risks highlights the necessity of a strategic approach to credit card use. For example, reviewing your credit card statements regularly and setting up alerts can help you avoid late payments and minimize the chances of falling into the trap of overspending.

Ultimately, the key to successfully building a credit history with credit cards lies in education and discipline. By being informed and cautious, you can harness the advantages of credit cards while steering clear of their potential downsides. This balanced approach will ensure that your journey toward a robust credit history remains productive and beneficial, setting the stage for a secure financial future.

Related posts:

How to Apply for the HSBC World Elite Mastercard Credit Card Today

How to Apply for Emirates Skywards Premium World Elite Mastercard Credit Card

Apply Easily for Choice Privileges Select Mastercard Credit Card Today

How to Apply for the HSBC Premier World Mastercard Credit Card

How to Apply for Bank of America Premium Rewards Elite Credit Card

How to Apply for Delta SkyMiles Platinum American Express Credit Card

Beatriz Johnson is a seasoned financial analyst and writer with a passion for simplifying the complexities of economics and finance. With over a decade of experience in the industry, she specializes in topics like personal finance, investment strategies, and global economic trends. Through her work on Dicas e Curiosidades, Beatriz empowers readers to make informed financial decisions and stay ahead in the ever-changing economic landscape.